Key Takeaways

- Owner financing allows buyers to bypass traditional lenders and negotiate terms directly with the seller.

- Buyers benefit from more flexible qualification criteria, but must be aware of higher interest rates and balloon payments.

- Understanding legal documents and conducting due diligence are vital for a smooth transaction.

- Legal guidance and tax consultation ensure both parties are well protected and aware of their obligations.

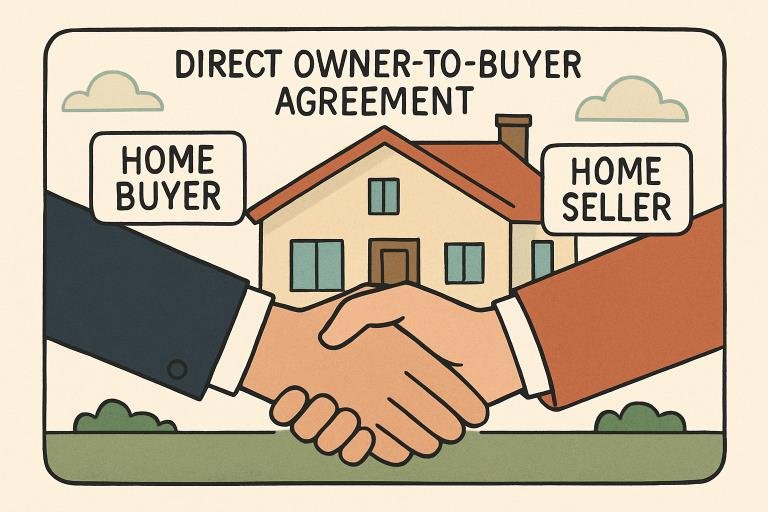

Understanding Owner Financing

Owner financing, sometimes called seller financing, is a real estate arrangement in which the property seller acts as the lender, allowing the buyer to make payments directly rather than through a traditional bank or mortgage company. This type of transaction can be especially helpful for those who face hurdles with conventional financing, such as recent changes in employment, self-employment, or credit issues. For buyers looking to purchase a home without bank approval, exploring https://www.cimarealestatetx.com/owner-finance-homes-in-richardson-tx/ can be a useful starting point.

Owner financing agreements are adaptable and often appeal to buyers interested in unique properties or challenging real estate scenarios that don’t fit standard loan requirements. Both parties negotiate the terms—including the interest rate, down payment, and agreement length—allowing for creative solutions tailored to their needs.

Many buyers are drawn to owner financing for its flexibility and the opportunity to build a relationship with the seller rather than a faceless institution. By removing the need for bank approvals and lengthy underwriting processes, owner financing can lead to smoother and faster home purchases.

Key Components of an Owner Financing Agreement

Promissory Note

The promissory note is the backbone of any owner financing agreement. It details the amount borrowed, the interest rate, the repayment schedule, and the processes used in the event of default. This document acts as the buyer’s commitment to repay the seller.

Deed of Trust or Mortgage

To protect the seller, a deed of trust or mortgage is recorded against the property, giving the seller the right to foreclose if the buyer defaults. This legal safeguard ensures the seller retains some control throughout the agreement. For more insights on owner financing structures, visit https://www.cimarealestatetx.com/.

Down Payment

Most sellers require a substantial down payment—often 10% to 20% of the purchase price. This upfront payment demonstrates the buyer’s commitment and reduces the seller’s risk. The exact amount is negotiable based on the property and the parties’ needs.

Interest Rate and Repayment Terms

Seller-financed deals frequently carry higher interest rates than traditional mortgages to compensate for increased risk. Repayment terms are customizable—some agreements have shorter durations, interest-only periods, or require a balloon payment at the end.

Advantages for Buyers

- Flexible Qualification:Owner financing is often accessible to buyers with less-than-perfect credit because sellers may not adhere to strict bank lending guidelines.

- Speed of Transaction:With fewer hurdles and paperwork, deals can close much faster, granting buyers quicker access to their new property.

- Lower Closing Costs:Buyers can save substantially on fees like appraisals, loan origination, and other charges imposed by traditional lenders.

Potential Risks and Considerations

- Higher Interest Rates:Compared to market averages, these deals frequently feature elevated interest rates, which can increase the total cost over time.

- Balloon Payments:Many owner-financed deals conclude with a large lump sum payment after a shorter payment term. Buyers must be prepared to secure a traditional mortgage or pay cash when the balloon payment comes due.

- Due-on-Sale Clause:When a seller has an outstanding mortgage, the lender may trigger a due-on-sale clause, requiring full loan repayment upon sale. This clause can pose a risk for buyers if not properly managed.

Steps to Secure an Owner Financing Agreement

- Assess Financial Readiness:Understanding your budget and monthly payment capability is a critical first step. Evaluate all upfront and ongoing costs, including potential increases if a balloon payment is required.

- Negotiate Terms:Open communication with the seller is key. Agree on interest rate, repayment schedule, loan length, and special conditions or clauses.

- Perform Due Diligence:To safeguard your investment, it’s essential to study the property’s fair market value, check for overdue taxes, assess its physical condition, and verify that the title is clear of liens.

- Engage Professionals:To minimize legal exposure and misunderstandings, retain a real estate attorney to draft and review all contracts.

- Close the Deal:Once you are satisfied with the documentation and terms, finalize the transaction and record all appropriate documents.

Legal and Tax Implications

Properly structured owner financing agreements protect both parties and may allow buyers to deduct mortgage interest on their federal taxes, similar to traditional home loans. However, state-specific laws and IRS rules must be considered. Always consult a tax professional to clarify your obligations and benefits when using owner financing.

Final Thoughts

Owner financing can open doors for buyers who face traditional lending roadblocks, offering flexibility, fewer up-front costs, and a faster path to homeownership. Yet, with these benefits come increased responsibilities—diligence, clear negotiation, and professional guidance are all essential to secure a safe, beneficial agreement. By understanding these key elements, buyers can more confidently approach the process and leverage owner financing when the right opportunity presents itself.